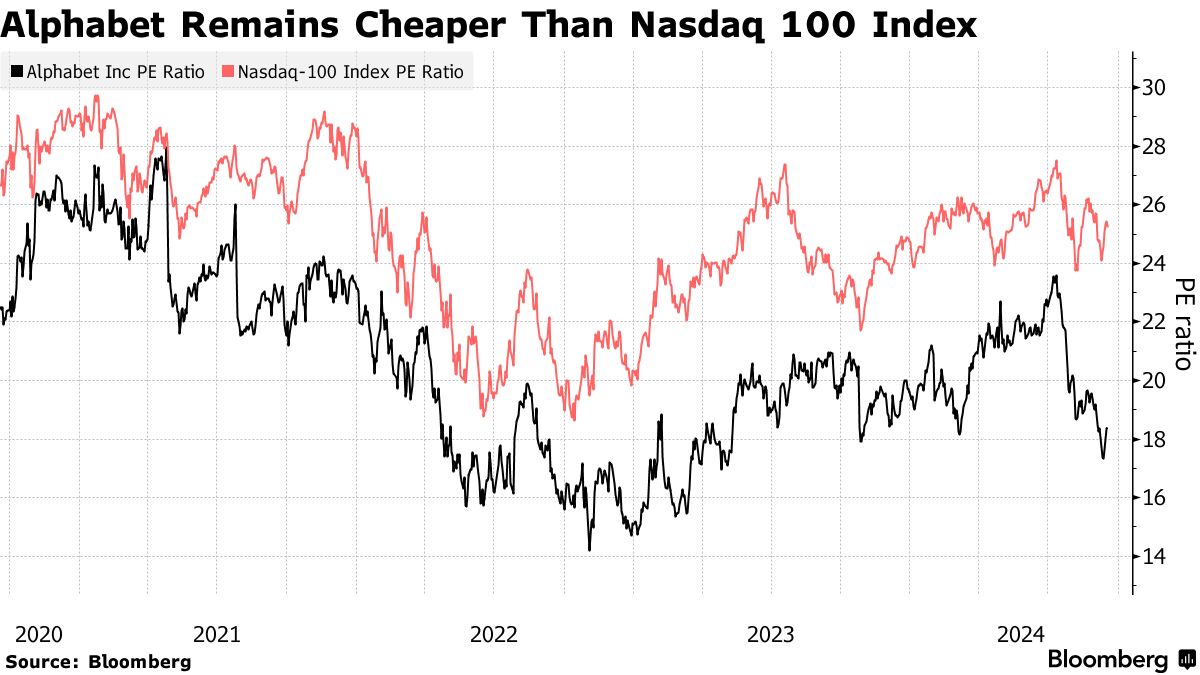

- Valuation is below historical average and overall Nasdaq Index

- Some investors say regulatory issues are priced in to shares

Gift this article

In this Article

Follow

Follow

Follow

Follow

Follow

Have a confidential tip for our reporters? Get in TouchBefore it’s here, it’s on the Bloomberg Terminal LEARN MORE

By Ryan Vlastelica and Subrat Patnaik

September 17, 2024 at 17:59 GMT+7

Updated on

Save

Listen

4:29

Alphabet Inc. shares have been struggling for the past two months amid mounting regulatory uncertainty. For some bulls, that’s a buying opportunity.

The Google parent’s stock price has fallen more than 20% from a July peak, and recently closed at a six-month low. While most Big Tech names have partially recovered from a summer rotation out of the sector, Alphabet has continued to fall. In August, a federal judge ruled that Google illegally monopolized the search market, with Bloomberg News later reporting that a bid to break up the company is one option being considered by the Justice Department.

“Alphabet is the only name in the Magnificent 7 to trade at what we consider a discount, and it is a significant discount,” said Gregg Abella, chief executive officer of Investment Partners Asset Management. “I’m not saying the regulatory issue isn’t a concern, because these cases can go on for a long time and no one knows how to handicap the outcome, but it has presented an opportunity.”

The share-price drop has left Alphabet trading at around 18 times forward earnings, cementing its place as the cheapest stock among the Magnificent 7. It also trades at a discount to its long-term average and the overall Nasdaq 100 index, which is trading at 25 times. Shares in the search giant edged higher, rising 0.6% on Tuesday.

“It’s getting to the point now where the valuation is starting to overwhelm the overhang,” said Eric Clark, portfolio manager at Accuvest Global Advisors, who said he bought back some shares in Alphabet last week after trimming his stake about six weeks ago. “I’m feeling much better about getting paid to absorb some of that risk and volatility at the current valuation.”

The antitrust issues in the US — and in Europe, where Alphabet recently lost a court case over a $2.6 billion fine related to shopping services — have caused some jitters on Wall Street. Morgan Stanley recently cut its Alphabet price target to $190 from $205, saying that antitrust-related uncertainty will put a narrow — and lower — band on the multiple.

Evercore ISI’s Mark Mahaney also cut his price target because of concerns around antitrust trials and potential remedies. Still, Mahaney remains bullish, saying that even in a worst-case scenario where Google is no longer allowed to bid for exclusive search distribution deals in the US, the related reduction in traffic acquisition costs would go a long way to offset this.

“Put it this way, Google could lose as much as 60% of its exclusive deal search revenue and still suffer only a single digit percentage loss in EPS,” he wrote, reiterating an outperform rating on the shares.

| Read more about antitrust issues facing Alphabet: |

|---|

| Google Almost Cut Ad Exchange Fees Ahead of Antitrust Crackdown |

| Google’s Ad Empire Under Fire as US Antitrust Trial Begins (1) |

| Apple, Google Defeats to Fuel EU’s Crackdown on Big Tech |

The regulatory issue comes as investors increasingly question how much companies like Alphabet are shelling out on AI, and when this spending will begin to pay off. Some investors are also concerned about Google facing more competition from the likes of OpenAI and Microsoft Corp. as they try to draw people away from traditional web search and toward chatbots that can answer users’ questions.

These issues may explain why Alphabet is relatively less liked than some megacap peers. Roughly 83% of analysts recommend buying the stock, compared with rates above 90% Nvidia Corp., Microsoft Corp. and Amazon.com Inc.

Still, Wall Street firms aren’t slashing their estimates on antitrust risk so far. The consensus for Alphabet’s 2025 revenue has risen by 6.6% over the past three months, according to data compiled by Bloomberg, a sign of continued optimism about the company’s prospects despite the risk of antitrust remedies.

“I think the regulatory issue has been priced in,” said Jason Britton, chief investment officer of Reflection Asset Management. “I virtually guarantee it will see more fines, but it has so much cash on its balance sheet that they won’t be material. This is really just a slap on the wrists.”

Top Tech Stories

- Intel Corp. Chief Executive Officer Pat Gelsinger has landed Amazon.com Inc.’s AWS as a customer for the company’s manufacturing business, potentially bringing work to new plants under construction in the US and boosting his efforts to turn around the embattled chipmaker.

- Microsoft raised its quarterly dividend 10% and unveiled a new $60 billion stock-buyback program, matching the size of a repurchase plan three years ago.

- The Hong Kong government is preparing to issue its maiden policy statement on the use of AI in finance, according to people familiar with the matter, a move that could catalyze the use of the technology in areas from trading to investment banking and cryptocurrencies.

- Lenovo Group Ltd. started building AI servers in India’s south, the latest boon for the rapidly growing country’s push to become a high-tech powerhouse.

Earnings Due Tuesday

- No major earnings expected

(Updates with stock move in paragraph four.)